It’s pretty easy to get started investing. Once you dig into it, though, a lot of questions come up that complicate the process. You might have come across the phrase alternative investments, and if you’re new to investing, you probably have no idea what it means. Here’s a quick breakdown for the average personal investor.

Illustration by Sam Wooley.

What is an “Alternative Investment”?

Let’s say you’re invested long-term for your retirement. You have a superannuation account that does all the work for you, or you have a fair mix of stocks and bonds in mutual funds. Either way, you’re already doing pretty well for yourself.

As your net worth grows, though, it’s time to take your portfolio up a notch. You want to diversify it even more, because, over time, a diverse portfolio is a lucrative one. A properly diversified portfolio includes different types of stocks and bonds — international stocks, for example — and it also includes something called alternatives. Elliott Weir, Founder & Certified Financial Planner at III Financial tells us why they’re important.

Alternatives can be useful in a portfolio to provide some balance. Often (but not always) when stocks and bonds drop, assets like commodities and real estate may rise. “Alternative asset” is a broad term that includes assets that are not stocks, bonds, or cash. Examples would be commodities (like gold), hedge funds, collectibles, and real estate. Often they are more complex assets that are more difficult to value and harder to turn into cash.

So technically, your old collection of Beanie Babies counts as an alternative. However, to invest in alternatives properly, it helps to understand how they work in a little more detail.

Why You Should (and Shouldn’t) Invest in Alternatives

If you’re just starting out with investing and playing catch up with your retirement, you might not be that interested in alternatives. You just need to focus on saving and building a simple set-and-forget portfolio. When your net worth starts growing, though, it might be time to squeeze alternatives into your portfolio. Financial Samurai’s Sam Dogen explains why:

With a larger net worth, you invest some of your savings into Alternative asset classes by age 35. Alternative asset classes may include: private equity, venture capital / angel investing, or starting your own company. You’ve got stocks, bonds, and real estate down pat. With free liquidity, you dable into the unknown because you never want to look back and say, “what if.”

After the age of 40, you’re looking for a more balanced mix in your net worth. As a result, you purposefully invest less in stocks and more into bonds and alternative investments. Your real estate equity also holds steady, market willing.

This is important: Alternatives aren’t meant to replace your entire portfolio. They’re meant to enhance it. Some investors will invest strictly in alternatives, though, like hedge funds. Warren Buffett, considered to be the world’s greatest investor, reminds us that they’re not a great deal, according to CNBC:

During the financial crisis, Buffett bet the asset management company Protege Partners LLC $1 million that the S&P 500 will outperform a portfolio of hedge funds over the 10 years through 2017. Buffett said Saturday the index fund is beating the hedge funds by nearly 44 percentage points over 8 years.

When the stock market drops considerably, though, people tend to freak out and, against better judgement and statistics, sell their stock and turn to alternatives like real estate, gold or other commodities. While those investments can be fruitful, depending on the time-frame you’re looking at, they’re also volatile and probably not smart investments for your retirement.

For example, gold prices soared during the ’80s and the Great Recession, but the Motley Fool’s John Maxfield explains why this doesn’t paint a full picture:

But the problem in both of these cases is that the price of gold soon dropped as quickly as it had formerly climbed.

It was less than $600 an ounce by 1985. And since peaking in 2011, gold has lost more than a third of its value.

To benefit from these fluctuations, then, an investor would have to time the market — something we know to be dangerous, if not impossible, for the average investor to do successfully.

In other words, alternatives are great for hedging and balancing your portfolio when the market drops, but that’s it. You should have them in your portfolio, but again: They’re not meant to replace your portfolio.

Calculate How Much of Your Portfolio Should Be in Alternatives

Here’s a basic rule of thumb for how to calculate your asset allocation, that is, the amount of your money that should be invested in stocks versus bonds:

110 – your age = the percentage of your portfolio that should be stocks

That means if you’re 30, you’d put 80 per cent of your portfolio in stocks (110 – 30 = 80) and the remaining 20 per cent in lower-risk bonds. This is a good starting point, but it doesn’t account for alternatives. And most basic asset allocation calculators only include stocks, bonds and cash.

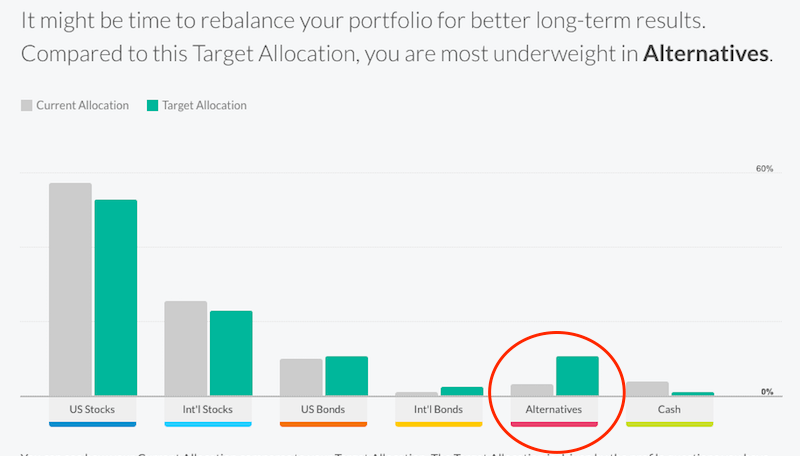

To find your alternative percentage, you could use an advanced portfolio checkup tool, like Personal Capital. You simply link your investment accounts, sort of like you would with Pocketbook, but instead of analysing your budget, Personal Capital analyses your portfolio and tells you what specific asset classes to invest in, including alternatives.

I use this myself, and the below image shows how much of my portfolio should be in alternatives compared to other asset classes:

If you’re looking for a simpler solution, here’s what Weir suggests:

In most cases, alternatives should not be a significant portion of a retirement investor’s portfolio. I recommend 3%-7% depending on several factors both because of their volatility and their relatively higher cost to own (vs. stocks and bonds).

The factors Weir mentions include your risk tolerance, other assets in your portfolio and how close you are to retirement. Ideally, the closer you are to retirement the less you want to invest in stocks. Your portfolio then shifts to bonds, but you may also want to invest in more alternatives to balance things out.

Types of Alternative Investments to Choose From

We’ve learned that alternatives are investments with a solid return made to hedge against stock market dips. That could be a lot of investments, but let’s go over a few of the most common.

Hedge Funds

In the past, alternatives weren’t really designed for the average, working class Jane just looking to save for her retirement. You’ve probably heard the term hedge fund, which is a traditional alternative investment.

When I think of hedge funds, I think of super wealthy people asking their financial advisors to move around millions of dollars. And that’s fair, because up until recently, hedge funds were complicated and crazy expensive, meant only for very rich people or institutions.

Hedge funds are made up of a variety of different alternative investments, sometimes they invest in startups, sometimes they use borrowed money and they’re designed to hedge against market volatility. In short, they ideally earn a return even when the market plummets, which keeps your portfolio balanced. These days, you can buy into a hedge fund the same way you would with a cheaper, exchange traded fund (ETF). Hedge funds aren’t the only alternative, though. We’ll get to more of them later.

Generally speaking, though, an alternative is an asset that’s independent of the market and earns a solid return over time even when the market drops.

ETFs and Mutual Funds

Again, hedge funds are traditional alternative investments, but hedge fund ETFs and mutual funds offer similar returns to the real deal. They may still require a large minimum investment, but it’s typically a lot more digestible than several million. Like regular mutual funds, these are made up of a pool of investments. In this case, these funds are meant to hedge the market.

Real Estate

Beyond those, real estate can be a decent alternative, and you don’t have to buy property to invest in it. Real Estate Investment Trusts (REITs) let you earn a return without becoming a landlord, and Weir suggests them as a starting point, too:

Start off with a low-cost mutual fund that focuses on alternatives, like Vanguard’s REIT Index Fund. This will leave the investment decisions up to a team that understands how that market functions. You can always find a fee-only CFP® planner to review what you own and/or make recommendations in your best interest.

Precious Metals

You could also invest in commodities, like gold or silver. Like REITs, most major investing firms like Vanguard have some kind of precious metal fund you can buy straight from your investment account. Fidelity’s gold fund, for example, is FSAGX.

There are other creative options, too. You could try peer-to-peer lending using a tool like Lending Club. I have about one per cent of my portfolio invested in them, and the returns aren’t great, but others have better luck.

Like any investment, you want to know what you’re getting into, and that means checking the return of your alternative, its long-term performance and its fees. As Forbes explains, two per cent is a typical fee for those million dollar hedge funds. If you buy an ETF or mutual fund, though, the fee shouldn’t be that high. Most mutual funds and ETFs have fees of even less.

Overall, it’s about making sure your portfolio is balanced in something other than stocks and bonds. You want a return, and that might mean more risk, but that’s the beauty of a balanced portfolio: When one area fails, another has your back.

Comments

One response to “The Normal Person’s Guide To Alternative Investments”

I let someone much smarter than me manage my money. Only just starting out but I don’t have any background in economics. Let a nobel laureate in the field create a good plan and follow it.

Just put the money in interest and some in gold, propert and stable shares for a little diversification.