Your home is probably the most expensive thing you’ll ever own, and that expense goes beyond the closing price. There’s the cost of the house, but then there are other ongoing and upfront expenses that can catch you off guard. Especially if you’re a first time buyer, it helps to know what you’re getting into.

Zillow estimates that, on average, Americans pay about $US9000 ($12,383) a year in extra home ownership costs, but that varies depending on where you live, and how you buy. Realestate.com.au estimates the extra costs of buying a $500,000 home in Australia to be $11,540″$14,050. Some of these costs aren’t exactly “hidden” but they are commonly overlooked. Let’s take a look at them in detail.

Home Inspections

You put an offer on a home, and it got accepted. Hooray! From here, inspections will be your first major expense. Yes, there may be more than one inspection.

Before you officially close on your house, you’ll want to schedule a thorough inspection. At a minimum, you want to order a general inspection of the house and an inspection for wood-destroying insects (also known as termites), if that’s not included in the general. A general inspection will run you a few hundred bucks, and a termite will probably be around a few hundred as well. Depending on the age and condition of the house, you may also want to schedule a sewer inspection, which can be another couple hundred dollars.

All of these can add up to over a thousand dollars, but that’s a small price to pay to make sure you’re not getting a lemon. If the house requires a hefty amount of maintenance, you might renegotiate with the seller, pull out of the deal completely, or simply budget for the added expense.

Even if another party has previously had the property inspected, it’s always a good idea to get your own inspection. It’s a big purchase, so it’s better to err on the side of caution. Plus, you want to be around during the inspection to see things for yourself.

You may need to pay survey costs, too. That can be another few hundred bucks, but you’ll get a professional survey of your property so you know exactly where your boundaries are.

Closing Costs

After your offer is accepted, your lender will crunch some numbers and run the paperwork. At this point, they should give you a detailed list of what your closing costs are. According to Zillow, closing costs will run you an extra 2 per cent to 5 per cent of the home purchase price. So if you’re buying a $200,000 home, expect to spend between $4000 and $10,000. Here’s what these costs usually include:

- Lender fees: These include everything from administrative costs to bank transfer fees.

- Appraisal: The home appraisal can be a big expense, at several hundred dollars. The lender wants to make sure the home appraises for the sale price.

- Title or attorney fees: Government filing fees, escrow fees, notary fees and any other expenses associated with transferring the deed over to you.

- Escrow fees: You might be required to pay some of your property taxes and insurance into an escrow account upfront.

- Interest: You’ll have to pay interest that’s prorated from the date of your closing to the first of the following month.

You can always plug some numbers into a closing cost calculator to get a bit more specific idea of what you’ll pay, but in general, expect to spend several thousand dollars on top of your down payment when you close on your home.

Budget for Ongoing Taxes and Insurance

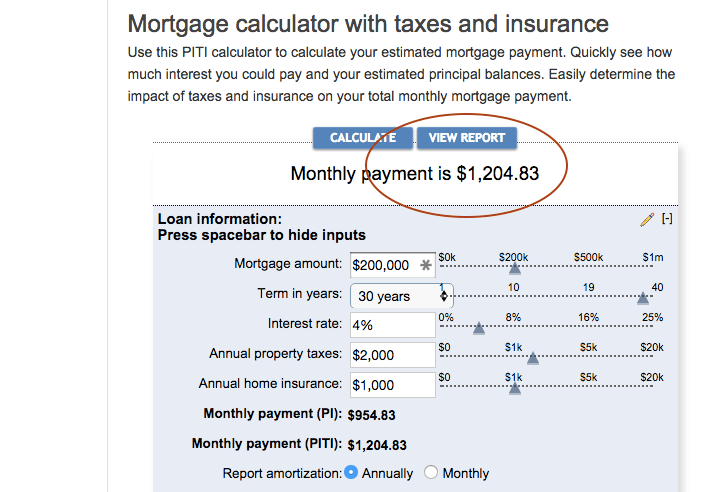

Monthly mortgage calculators tell you what your mortgage payment, including interest, will be each month. They don’t always include the taxes and insurance, though, and that adds up. For example, if you have a $200,000 mortgage at 4 per cent interest over thirty years, your mortgage and interest will be $954. Not too bad. But calculate your total monthly mortgage principal, interest, taxes and insurance. (PITI), and here’s what your payments look like:

When calculating your monthly mortgage payment, include the cost of interest, taxes, and insurance (PITI).

That’s quite the jump! It doesn’t even include mortgage insurance, which you generally have to pay if your down payment is less than 20 per cent. That can range from 0.5 per cent to 1 per cent of the cost of your loan.

Of course, your taxes will vary depending on the value of your home and where you live, but will likely be several thousand dollars.

Depending on the terms of your loan, you might pay this monthly into an escrow account. In this case, you make these payments to your lender, and they will pay your taxes and insurance on your behalf. If you don’t have an escrow account, you’ll just pay them on your own directly when they’re due.

However and whatever you pay, make sure to budget for this ongoing, recurring cost.

Keep Funds On Hand for Maintenance and Repair

When your air conditioning craps out as a renter, it’s a pain, but all you have to do is call your landlord and hope for the best. As a homeowner, it hurts a little more because you have to pay for for the repair yourself.

Most people know owning your own home means forking over the cash for your own maintenance, but you might underestimate how much these projects will run you. Jammed disposals, leaky faucets and cracked exterior paint are just a few repair projects that catch most first-time homeowners off guard.

Every home is different, so there’s no one-size-fits-all answer for determining how much you’re going to pay on maintenance every year. However, here’s what one financial planner told The New York Times, based on his own experience with clients:

Mr. Stearns estimates that owners of a newer home that do some work for themselves but contract major work out to others will pay 3.6 per cent of the original purchase price annually for maintenance and 4.5 per cent if it’s an older home.

Other sources put that number as low as one per cent. When dealing with money, it’s almost always a good idea to err on the side of caution though, so it can’t hurt to have about four per cent of the purchase price budgeted for repairs each year. For a $200,000 home, that’s about $8000. It seems like a lot, but even if you don’t spend that money, consider it an emergency fund for your home.

Prepare for Higher Utility Bills

Let’s say you moved out of your cramped apartment and into a nice, three-bedroom home. Elbow room is great, but it also means your bills will be a little higher.

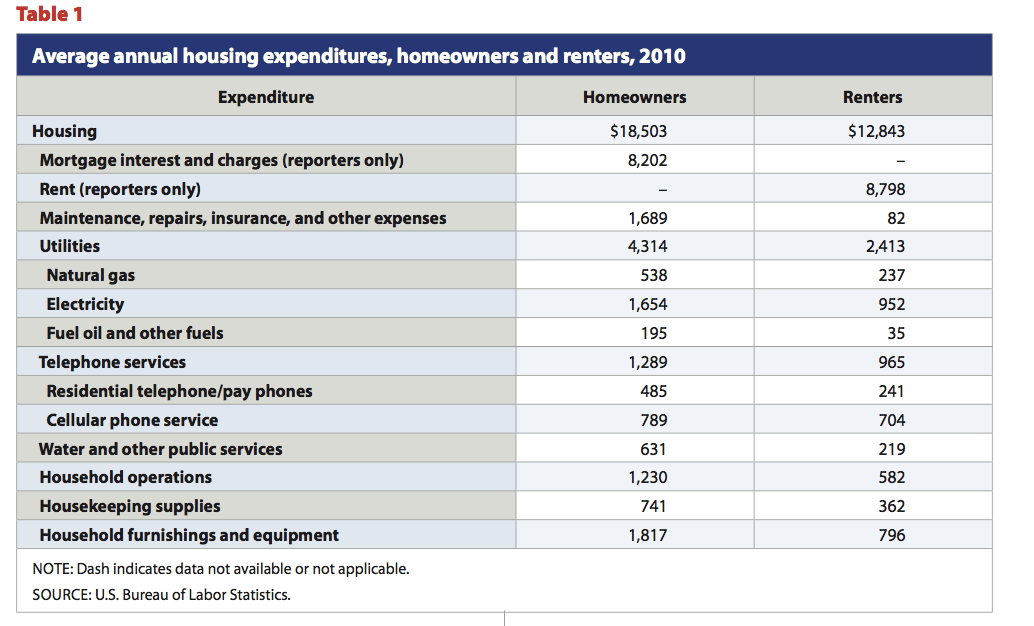

Depending on what you’re used to paying, your gas, electric and water bills won’t necessarily be higher when you buy a home, but they often are. Plus, your landlord might foot the bill for some expenses (like trash pickup or water) that you’ll have to pay when you own. According to the latest data from the US Census, homeowners pay a couple of thousand dollars extra on utilities every year, compared with renters, and you can expect the numbers in Australia to be similar. Here’s the breakdown:

Average expenses for homeowners versus renters, according to the Bureau of Labour Statistics.

Of course, this is an estimation based on national data, so once again, your own numbers will vary. To get an idea of what your own situation will look like, home site Money Pit suggests asking the seller if you can take a look at their past bills:

Your realtor can arrange this through the seller’s realtor, or, in the case of a house for sale by owner, ask the seller directly for the tally. Use this information as a guide, remembering that year-to-year changes in climate conditions and energy use patterns by a new combination of residents will lead to variations.

It might be a long shot, but it’s probably the easiest way to see how much you’ll pay. You could also order a home energy audit. This basically involves an auditor inspecting your home to tell you how to improve its energy efficiency. This will run you several hundred dollars, though. You can do a general one yourself by checking your insulation, looking for air leaks and possibly replacing some appliances and A/C systems.

Buying a home is traditionally thought to be a smarter financial decision than renting. The argument is that, when you rent, you’re throwing money away, but when you buy, you own your home at the end of the day. Sure, if you compare rental price to the bare bones price of your mortgage, that may be true. However, all of these extra costs add up. And, like your rent, those expenses don’t exactly buy you anything: they’re just the price you pay for owning.

Still, even with these costs, buying is a better long-term financial decision than renting in many areas. You want to crunch the numbers yourself, considering all of these unexpected costs. (The New York Times rent vs. buy calculator is probably the best tool we’ve seen for crunching these numbers.)

At any rate, once you make your decision to buy a home, be prepared for the price you’ll really pay. Factor in these expenses, and you should be on track.

This story has been updated since its original publication.

Comments

3 responses to “All The Hidden, Unexpected Costs Of Buying A Home”

As an extra regarding maintenance and repair, if you buy a new property, dont assume you’ll be immune to those costs. New properties need to settle, and get into their own groove, so to speak, which can mean pipes come loose, or wiring may be a little off, or some other small thing that needs work.

A lot of the time its not going to be covered by the builder, or its simpler sorting it yourself, and means you’re out of pocket, and it could be for anything.

I bought new about 9 years ago and in the first 6 months had to get an electrician in, and a plumber, because of small things that wouldnt have been picked up earlier. Well, one should have, but it was easier to just get it done.

On the whole though, after a few teething issues, you should be good for a decade or more if the builder knew his job. Just be ready for teething problems.

Building a house is even worse. Concreting and landscaping is just the start.

Our builder had a small footnote on our plans that said”may need retention”. Having had to build our slab up with about 100 tonnes of dirt (at extra cost) so the sewage drained to the front of the block, we then had to retain the entire Eastern fence line. Neighbour didn’t want a part of it and it cost us an extra 15k just for a retaining wall. Said neighbour even then tried to tell me I needed to pay the additional cost of putting a fence on the wall as opposed to the ground. Regardless of the fact I had previously told him a wall would be there when the fence was going to be built. I said I wasn’t going to pay the extra $1200 so we had the cheapest and nastiest fence you’ve ever layed eyes on.

Furniture was ours, we went from a 1 bed flat with hand me down mismatched furniture to needing to fill a 3 bed house! Spent about $20k on beds, sofas, bookshelves, technology etc!

Probably tools is another hidden expense if you’ve come from an apartment into a house, might need a mower, ladder, shovel, rake etc.

Probably best to factor in extras when buying a house, don’t go for the absolute maximum mortgage you can afford.