Target date funds, also known as lifecycle funds, look like easy set-and-forget ways to save for retirement. They do all the work of diversifying and reallocating your funds for you. But if you’re investing outside of your target date fund, you might be shooting yourself in the foot.

Image via JP Morgan Chase.

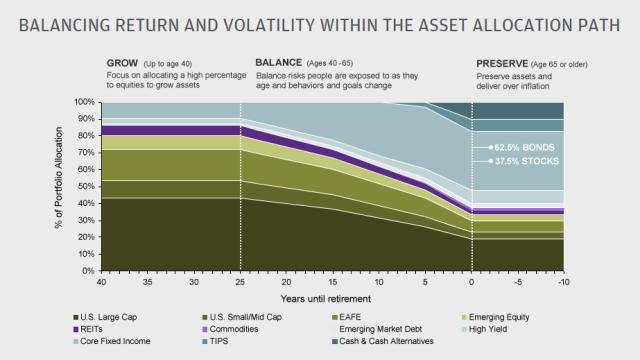

Lifecycle or target date investment options are increasingly popular in Australia. According to statistics from Australian Prudential Regulation Authority (APRA), nearly 30 MySuper funds have lifecycle investment strategies as their default option.

But a lot of people who use a target date fund may not be fully invested in them. They buy additional mutual funds or stocks. Some of them cited: To further diversify, to invest more aggressively and to have more control.

But target date funds are designed with a particular diversification strategy in mind, and if you pick up other investments, you could be over- or under-weighing your investments in certain sectors, geographic regions and so on.

Target date funds might be riskier than you think on their own, but they’re even riskier if you combine them with other investments. According to Financial Engines’ chief financial officer, Christopher Jones, people who partially invest in target date funds get returns that are two per cent less per year than those who use only target date funds.

Money Magazine recommends that investors still need to look at their full financial circumstances in choosing the most suitable fund.

Target-Date Mutual Funds Are ‘Not So Simple’ — Financial Engines CFO [The Street]

Comments